Global Opportunities for Relocation: a summary of tax regimes around the word

Global Opportunities for Relocation: a summary of tax regimes around the word

Relocating abroad has increasingly become a strategic decision for wealthy individuals and their families, rather than a one-off change of residence. Motivations vary widely – from lifestyle considerations, education and healthcare, to access to new markets or long-term wealth diversification. Greater flexibility in working arrangements and the ability to maintain homes in multiple countries have further accelerated this trend.

From a long-term perspective, however, one factor consistently proves decisive: the tax framework applicable after relocation. A lack of clarity around tax residency, the scope of taxable income or reporting obligations can lead to unexpected exposure and inefficiencies. Understanding the tax landscape early is therefore essential to maintaining financial certainty.

Why the tax regime is critical when relocating

Although tax is rarely the sole reason for relocating, it plays a critical role in ensuring predictability and stability once the move has taken place. Countries adopt fundamentally different approaches to taxing individuals, and these differences go far beyond headline tax rates.

In practice:

-

some jurisdictions tax worldwide income of tax residents,

-

others focus primarily on domestic-source income,

-

some apply specific regimes or preferential treatment for new residents or certain categories of individuals.

As a result, individuals with a comparable income or asset profile may experience very different tax outcomes depending on where they relocate.

Key tax regimes encountered in relocation planning

When assessing jurisdictions from a relocation perspective, personal tax systems generally fall into several broad categories. These categories reflect how countries approach the taxation of income and gains rather than isolated incentives.

-

Low tax / No tax

Some countries apply very low or no personal income tax, or significantly limit the scope of taxable income. These regimes can be attractive for internationally mobile individuals, particularly those with foreign-sourced income, but require careful consideration of tax residency rules and ongoing compliance obligations.

-

Rremittance basis

Under a remittance basis approach, foreign income and capital gains are not taxed automatically. Taxation depends on whether, and to what extent, such income is brought into the country. Managing cash flows, timing and the definition of remittances is therefore a key consideration.

-

Favourable for new residents

Certain jurisdictions provide tax incentives to individuals who relocate and become tax resident. These may apply to passive income, capital gains, pensions or employment income and are often subject to time limits or specific conditions.

-

Lump sum taxation

Some countries allow individuals to agree a fixed annual tax liability, irrespective of actual income earned or gains realised. While this offers a high degree of predictability, eligibility is typically subject to clearly defined criteria.

-

Standard taxation regimes

Other jurisdictions do not offer relocation-specific regimes and apply their general domestic tax rules to resident individuals.

Different mechanisms, common objectives

While the design of these regimes varies, they share a common objective: determining how income is taxed based on its source, the individual’s connection to the country and the nature of their activities.

In practice, this often results in a combination of:

-

territorial elements within personal tax systems,

-

targeted exemptions for specific income types,

-

differentiated treatment of domestic and foreign income.

Understanding how these mechanisms interact is critical when evaluating the overall tax position following relocation.

Regional differences influencing relocation decisions

From a global perspective, regions offer distinct combinations of lifestyle and tax considerations:

-

The Americas continue to attract individuals due to economic opportunity, political stability and access to education and healthcare, with tax systems varying significantly by country and residency status.

-

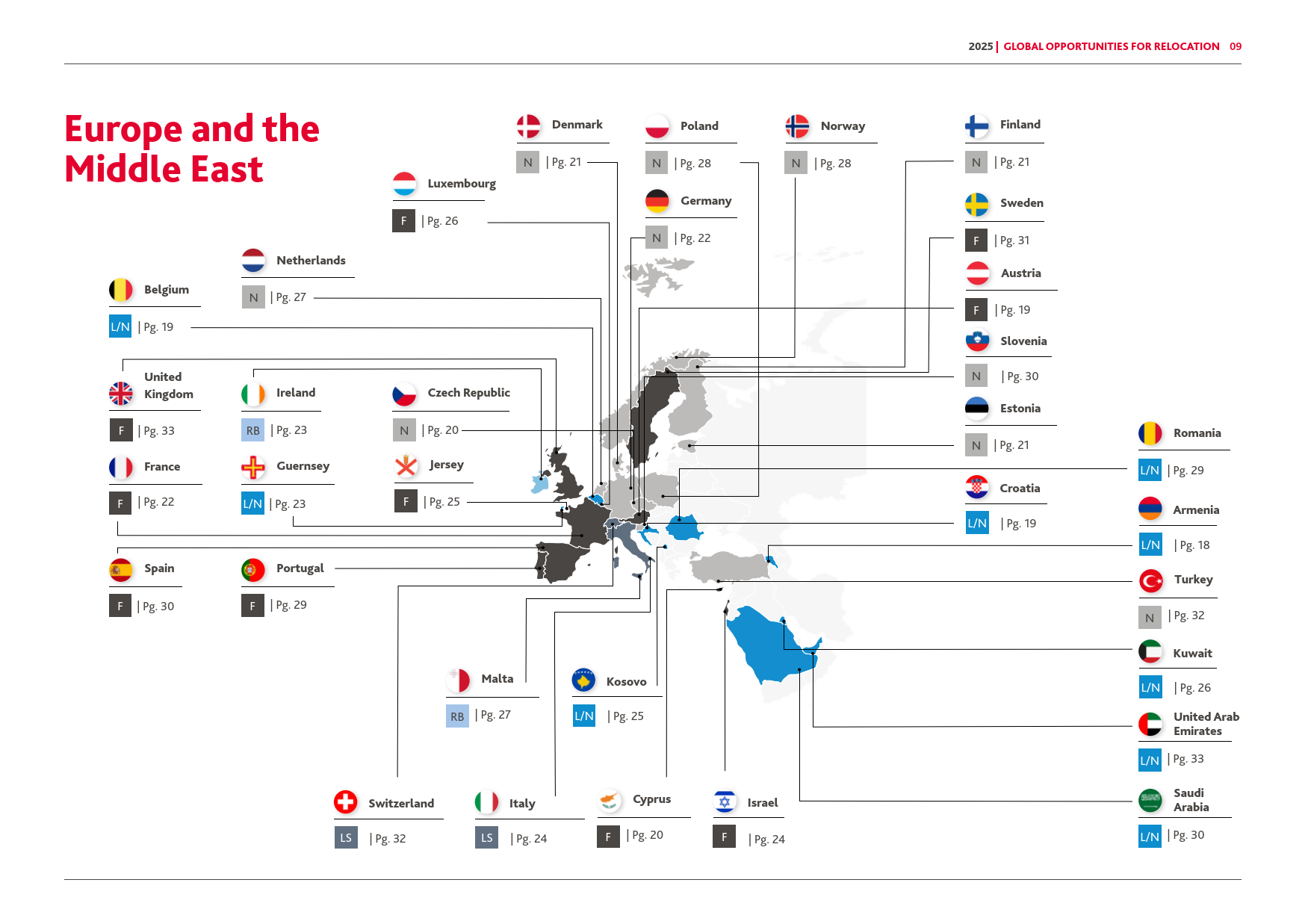

Europe offers a wide range of approaches, from lump sum regimes to targeted incentives for new residents, alongside a high standard of living and strong infrastructure.

-

Asia and the Middle East attract entrepreneurs and high-net-worth families through a combination of low tax environments, dynamic growth and established financial centres.

There is no universally “best” location. Suitability depends on personal circumstances, income structure and long-term objectives.

Relocation as a structured process

Experience shows that relocation should be approached as a process rather than a single step. Beyond tax residency itself, it is important to consider:

-

ownership and asset structures,

-

the impact of residency on companies, trusts or employers,

-

succession planning, inheritance and international wills,

-

the timing of the move.

Early planning significantly reduces the risk of unexpected tax consequences and the need for later corrective action.

How BDO supports clients with relocation

Through its global network, BDO advises individuals, entrepreneurs, families and family offices on tax and related matters connected with international relocation. Our focus is on:

-

understanding local tax rules in relevant jurisdictions,

-

identifying an appropriate tax framework aligned with the individual’s situation,

-

ensuring consistency and compliance across borders.

Our objective is to help clients approach relocation with clarity, predictability and long-term tax sustainability.

Conclusion

Relocating abroad opens up new opportunities, but it also brings complex tax considerations. Differences in personal tax regimes can have a significant impact on long-term financial outcomes. Decisions grounded in a clear understanding of the applicable tax framework are invariably more robust than solutions addressed retrospectively.